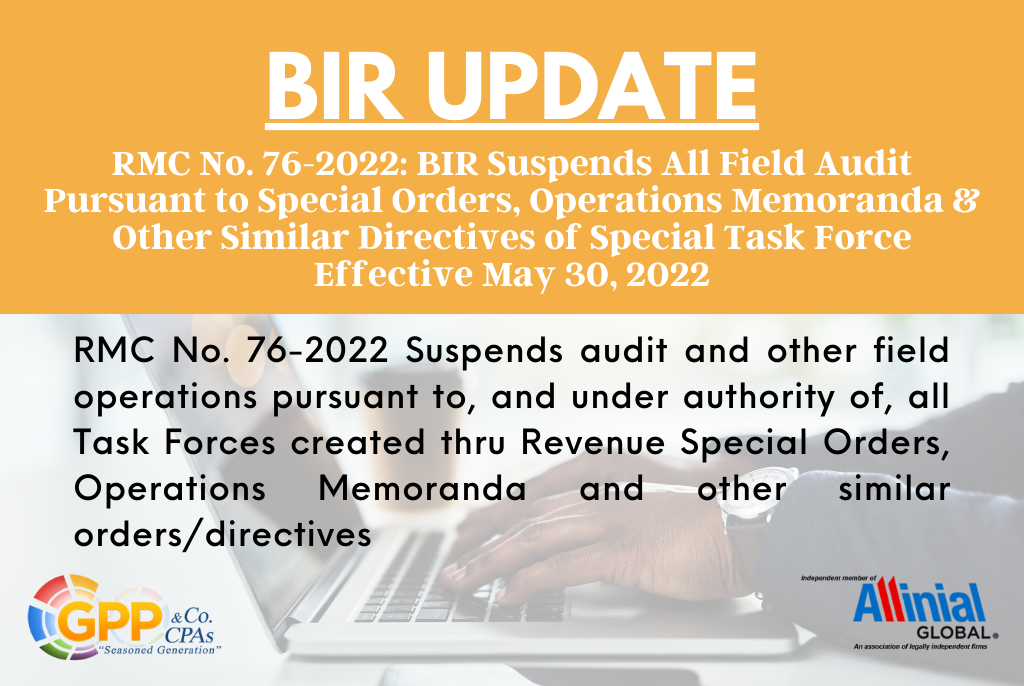

RMC No. 76-2022: BIR Suspends All Field Audit Pursuant to Special Orders, Operations Memoranda & Other Similar Directives of Special Task Force Effective May 30, 2022

super_admin2022-06-13T02:15:11+08:00On May 30, 2022 BIR Issued the Revenue Memorandum Circular (RMC) NO. 76-2022, to suspends until further notice all field audit of the BIR pursuant to, and under authority of, all Task Forces, created thru Revenue Special Orders (RSOs), Operation Memoranda (OM), and other similar orders or directives, relative to examinations of taxpayers’ books of account and accounting records effective May 30, 2022. As such, no field audit, field operations or any form of business visitation in the execution of Letters of Authority/Audit Notices (LOAs) or Mission Orders (MOs) should be conducted by the said Task Forces. All reports must be [...]